Poland: Balancing Market Reform - Electricity

-

Legal Development 27 March 2024 27 March 2024

-

UK & Europe

-

Energy & Natural Resources

The Balancing Market Reform, set to launch in June 2024, is expected to become a significant transformative force within the electricity community. Its impact will eventually be experienced by every user of the system, but it is the generators, traders and balancing responsible parties (BRPs) who are at the forefront of this reform. The Battery Energy Storage System (BESS) investors also hold great expectations for the potential benefits this reform may bring.

What will it bring?

Upon the launch of the Balancing Marketon 14 June 2024, it will be organized around two primary streams - imbalance settlements and balancing services, in accordance with a standardised approach outlined in the EU Electricity Balancing Guideline (EB GL). Market activities will cover each delivery day, initiating on a day-ahead basis and continuing throughout the day in question.

All system users are involved in imbalance settlements, either through direct participation or the appointment of a BRP, assuming responsibility for the difference between scheduled and actual generation (discharge) or consumption (charging). Exposure to imbalance cost will now include a possible spread between long and short position pricing, reflecting the impact on the system. Imbalances will be tracked and settled at 15-minute intervals.

In order to provide balancing services, a separate certification as a balancing service provider (BSP) and as an aggregator will be required. There may not be a choice for every BRP, neither will every BSP manage and settle imbalances. Depending on your role and goals in the electricity market, selecting the right partner is crucial.

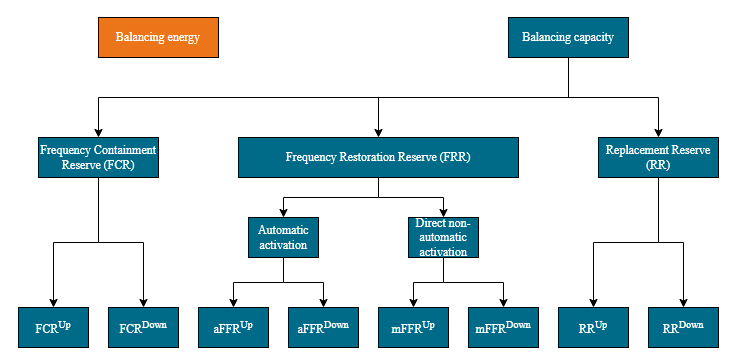

Balancing services include balancing electricity and various types of services based on capacity. In alignment with the EU framework, market participants will identify these services as FCR, FRR and RR . Each service will involve upward and downward regulation, and FRR will be additionally split into automatic (aFRR) and manual (mFRR) response variants.

Poland is yet to join the European common procurement platforms, at the initial phrase of the reform, capacity-based services will maintain their domestic nature. The operational reserve will continue to provide the standard suite of services.

The rollout

The roll out was started in February 2024 with the setup of communication interfaces between the TSO and Balancing Market participants. Before the end of May, there will be a phase of functional integration testing, and a dry run using a live set of data to demonstrate differences and test functionalities between the old and new systems.

Market participants, in particular the BRPs and BSPs, must be prepared to commence operations in the new framework from 13 June 2024 and 14 June 2024 will be the first day of deliveries resolved under new Balancing Market rules. It will be mandatory for certain classes of system to provide balancing services.

Renewable generators connected to the PSE’s transmission network are expected to take action to ensure the compliance of the transitional and long-term waivers in advance of the launch date.

How might this impact your business?

It is vital for the industry players to address a reform of such importance, in particular to consider its impact on their existing contractual relationships and revenue models. Despite the fact that imbalance settlements are already included in any standard market access setup, the experience of other markets indicates until first lessons are learned, it is likely to cause an increased volatility of pricing and therefore higher balancing cost. This in turn could lead to settlement or contract adjustment, depending on specific arrangements with BRPs.

As a result of the reform, for those interested in providing balancing services the reform, a new setup is required – either taking on the role of a BSP, or identifying one with whom to contract. Renewable generators should review the risk of potential curtailment (a phenomenon that from 2023 changed from a theoretical possibility to a genuine market experience) and how it could be mitigated through tailored terms of engagement with a BRP or BSP.

Background

Poland has historically developed a centralised balancing system with all key functions and responsibilities handled by PSE S.A., the sole Polish transmission system operator. This country-specific approach has heavily relied on the utilisation of balancing services from large scale fossil fuel generators, although there have been some recent opportunities for DSR providers.

A spread on imbalance prices existed in the past but was eliminated many years ago. This elimination, however, resulted in certain inconsistencies between the regular SPOT market (day-ahead and gradually developed intra-day) and the Balancing Market.

To address the inconsistencies, the current reform was initiated in 2020 but was postponed due to the pandemic and the 2022 energy crisis. Once implemented, it will bring the general setup of the Balancing Market in line with the standardised EU framework, particularly the Electricity Balancing Guideline (EB GL) and other relevant network codes.

End